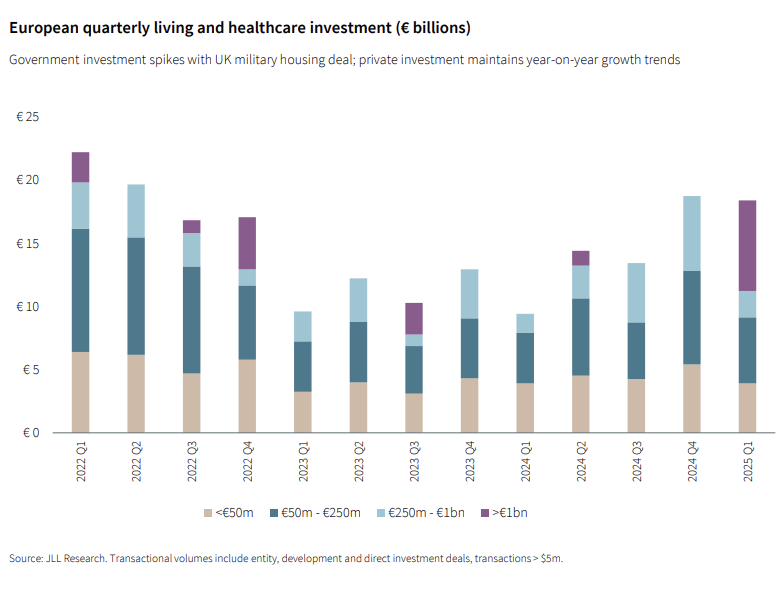

Residential investment volumes declined by 59% year-on-year, reaching €7.3 billion in Q1 2025—the lowest first-quarter figure since 2019. This decline is primarily attributed to lender caution, ongoing price corrections, and challenges in asset valuation.

Nevertheless, underlying demand for residential property remains robust. While investment activity has slowed, the fundamental drivers of housing demand are strengthening. These include limited housing supply across many European cities, rising migration flows, an increasing need for affordable rental options, and demographic trends such as population ageing in Western and Central Europe.

Strong demand for rental housing continues to support the performance of income-generating residential assets, even amid a subdued transactional environment. This resilience highlights the attractiveness of the living sector as a long-term investment opportunity, despite current market headwinds.

At the regional level, despite the overall market contraction, the United Kingdom and Germany remain the most active residential investment markets. In contrast, the Nordic region and Central Europe exhibit subdued investment activity, reflecting more cautious investor sentiment and market-specific challenges.

Institutional investors, such as pension funds and insurance companies—traditionally strong players in the residential space—remain active, though they are increasingly focusing on build-to-core and core-plus strategies, targeting assets with lower risk profiles and more predictable returns.

On the development side, new residential construction is constrained by elevated construction costs and regulatory bottlenecks, including delays and restrictions in permitting processes. These factors render many projects financially unviable, despite the presence of strong underlying demand. In addition, the high cost of capital continues to weigh on development pipelines, discouraging developers from undertaking new projects, even in supply-constrained markets.

At the same time, regulatory interventions in rental markets are becoming more common across European cities, adding a layer of uncertainty for investors—particularly in jurisdictions lacking a stable fiscal or legal framework. This evolving regulatory landscape raises concerns around rent controls, taxation, and compliance, potentially impacting long-term investment strategies.

A positive finding from the research is the increased participation of cross-border investors, particularly from the United States and Asia, who appear to be leveraging market volatility for strategic positioning. As a result, more "patient capital" is re-entering markets that are showing early signs of price stabilization, such as France and Spain.

Despite the short-term slowdown, JLL maintains that the residential sector across the EMEA region continues to offer strategic resilience underpinned by fundamental demand drivers. According to the firm's outlook, once macroeconomic indicators stabilize and financing costs normalize, investor interest is expected to rebound, particularly in emerging residential investment models such as build-to-rent, student housing, and co-living. These asset classes are viewed as having strong long-term potential to address evolving demographic and urbanization trends.

Source:JLL